International Public Sector Accountings Standards (“IPSAS”) Background

The International Public Sector Accounting Standards Board® (“IPSASB®”) is an independent standard setting board supported by the International Federation of Accountants® (“IFAC®”). The IPSASB issues IPSAS, guidance, and other resources for use by the public sector around the world. The IPSASB consists of 18 members, of which 15 are drawn from IFAC member bodies, and the remaining three are public members with expertise in public sector financial reporting. All members of the IPSASB, including the chair and deputy chair, are appointed by the IFAC Board on the recommendation of the IFAC Nominating Committee.

The development of the IPSAS has its origins in the accounting profession as a way to improve the transparency and accountability of governments and their agencies by improving and standardising financial reporting.

The IPSASB developed IPSASs which apply to the accrual basis of accounting and IPSASs which applies to the cash basis of accounting.

As transactions are generally common across both the private and public sectors, there has been an attempt to have IPSAS converged with the equivalent International Financial Reporting Standards® (“IFRS®”).

Majority of the IPSAS are aligned with IFRS. The format of IPSAS is similar to that of IFRS.

As a general rule, the IPSAS maintained the accounting treatment and original text of the IFRS, unless there is a significant public sector issue that warrants a departure. The IPSAS are also developed for financial reporting issues that are either not addressed by adapting IFRS or for which no IFRS has been developed.

IPSASB issued comprehensive Cash Basis IPSAS that includes mandatory and encouraged disclosure sections.

The IPSAS are intended to be applied in the preparation of general-purpose financial reports (“GPFRs”).

GPFRs are financial reports intended to meet the information needs of users who are unable to prepare financial reports tailored to meet their specific information needs.

IPSAS are aimed for application to the GPFR of all public sector entities other than Government Business Enterprises (“GBEs”). GBEs are expected to apply IFRS.

The IPSASB standard-setting activities follow a public due process. The process provides an opportunity for all those interested in financial reporting for the public sector to express their views to the IPSASB that are considered as part of the development of IPSAS.

IPSAS are authoritative standards on accounting for and reporting economic transactions and events in general purpose financial statements of public sector entities.

IPSAS have a general structure that includes an objective, scope, definitions, accounting and disclosure requirements, transitional provisions and effective date. The sections are generally self-explanatory. They may also include application guidance as part of the authoritative text.

When an IPSAS is based on IFRSs, it will be accompanied by a comparison which highlights the changes in accounting treatment and original text of the relevant IFRSs when there is a significant public sector issue which warrants a departure.

The development of IPSAS typically involves proposals being set out in an Exposure Draft (“ED”) that is released by the IPSASB for public comment. The due process allows for Consultation Papers (“CP”) to be issued prior to an ED to consider an issue in detail and provides the basis for further discussion and debate. The IPSASB also issues Recommended Practice Guidelines (“RPG”). Due process documents have finite comment periods.

IPSAS are issued as the final set of the due process and mark the conclusion of the IPSASB’s deliberations on a financial reporting issue. Subsequent amendments to an IPSAS require the due process to be followed.

Adaptation of IPSAS

An increasing number of governments and intergovernmental organisations produce financial statements on the accrual-basis of accounting in accordance with IPSAS or IPSAS-similar standards. The information contained in accrual accounting IPSAS financial statements is considered useful, both for accountability and for decision-making purposes. Financial reports prepared in accordance with IPSAS allow users to assess the accountability for all resources that the entity controls and the deployment of those resources, assess the financial position, financial performance, and cash flows of the entity and make decisions about providing resources to, or doing business with, the entity.

IPSAS 33 provides guidance to a first -time adopter that prepares accrual bases IPSAS. Features of a successful transition include:

- A clear mandate;

- Political commitment;

- Commitment of central entities & key officials;

- Adequate resources (human & financial);

- An effective project management structure;

- Adequate technological capacity and IT systems; and

- Use of legislation.

Users of GPFRs of public sector entities need information to support assessments of matters such as:

- Whether the entity provided its services to constituents in an efficient and effective manner;

- The resources currently available for future expenditures, and to what extent are restrictions or conditions attached to their use;

- To what extent the burden on future year taxpayers of paying for current services has changed; and

- Whether the entity’s ability to provide services has improved or deteriorated compared to the previous years.

IPSAS facilitates the alignment with best accounting practices through the application of credible, independent accounting standards on a full accrual basis. It improves consistency and comparability of financial statements as a result of the detailed requirements and guidance provided in each standard.

Accounting for all assets and liabilities improves internal control and provides more comprehensive information about costs that will better support results-based management.

The following benefits can be derived from adopting Accrual basis IPSAS:

- Reports all:

- economic resources controlled by entity.

- claims against economic resources.

- full cost of goods and services.

- Improves transparency and accountability.

- Provides better information for decision making.

- Improves consistency and comparability of reporting.

Criteria to apply IPSAS

IPSAS are designed to apply to public sector entities that meets all of the following criteria:

- Are responsible for the delivery of services to benefit the public and/or to redistribute income and wealth;

- Mainly finance their activities, directly or indirectly, by means of taxes and/or transfers from other levels of government, social contributions, debt or fees; and

- Do not have a primary objective to make profits.

For the purposes of IPSAS, the ‘public sector’ refers to national governments, regional governments (e.g., state, provincial, and territorial), local governments (e.g., town and city), and related governmental entities (e.g., Government ministries, agencies, programs, boards, and commissions).

IPSAS also applies to public sector social security funds, trust, statutory authorities and International governmental organisations.

Characteristics of public sector entities

The following characteristics of the public sector were considered by the IPSASB to develop the IPSAS:

- The volume of financial significance of non-exchange transactions: In a non-exchange transaction, an entity receives value from another party without directly giving approximately equal value in exchange. Such transactions are common in the public sector. The nature of non-exchange transactions may have an impact on how they are recognized, measured, and presented to best support assessments of the entity by service recipients and resource providers.

- The importance of the approved budget: Most governments and other public sector entities prepare budgets. In many jurisdictions there is a constitutional requirement to prepare and make publicly available a budget approved by the legislature (or equivalent). The approved budget is often the basis for setting taxation levels and is part of the process for obtaining legislative approval for spending. Reporting against budget is commonly the mechanism for demonstrating compliance with legal requirements relating to the public finances.

- The Nature of public sector programs and the longevity of the public sector: Many public sector programs are long term and the ability to meet commitments depends upon future taxation and contributions. The financial consequences of many decisions will have an impact many years or even decades into the future.

- The nature and purpose of Assets and Liabilities in the public sector: In the public sector, the primary reason for holding property, plant and equipment and other assets is for their service potential rather than their ability to generate cashflows. Because of the type of services provided, a significant proportion of assets used by public sector entities are specialized – for example, roads, military assets. There may be a limited market for such assets and even then, they may need considerable adaptation in order to be used by other operators. These factors have implications for the measurement of such assets.

Governments and other public sector entities may hold items that contribute to the historical and cultural character of a nation or region – for example, art treasures, historical buildings and other artifacts. Governments may also be responsible for national parks and other areas of natural significance with native flora and fauna. Such items and areas are not generally held for sale, even if markets exist. Governments and public sector entities have a responsibility to preserve and maintain them for current and future generations. - The regulatory role of public sector entities: Many governments and other public sector entities have powers to regulate entities operating in certain sectors of the economy, either directly or through specifically created agencies. Judgement may be necessary to determine whether such regulations create rights or obligations that requires recognition as assets or liabilities considering the government or public sector entities ability to amend such regulations.

- Relationship to statistical reporting: Many governments produce two types of ex-post financial information:

(a)Government financial statistics (“GFS”) on general government sector (“GGS”) for the purpose of macroeconomic analysis and decision making.

(b)General purpose financial statements (financial statements) for accountability and decision making at an entity level, including financial statements for the whole government.

Both IPSAS financial statements and GFS reports are concerned with:

(a) Financial, accrual -based information.

(b) Government assets, liabilities, revenue and expenses.

(c) Comprehensive information on cashflows.

| IPSAS objectives | GFS objectives |

| Accountability | Analyze fiscal policy options |

| Decision making | Making policy and evaluating the impact of fiscal policies |

| Determine the impact on the economy | |

| Compare fiscal outcomes nationally and internationally |

The removal of differences between the two accounting frameworks that are not fundamental to their different objectives and the reporting entities use of a single integrated financial information system to generate both IPSAS compliant financial statements and GFS reports can provide benefits to users in terms of report quality, timeliness and understandability.

Accounting Basis

IPSASB defines accounting basis to mean either the accrual or cash basis of accounting as defined in the accrual basis IPSAS or the Cash Basis IPSAS, respectively. The IPSASB encourages governments to progress to the accrual basis of accounting, and to adopt accrual basis IPSAS.

The cash basis of accounting recognizes transactions and other events only when cash is received or paid. Under the cash basis of accounting revenue is recorded when cash is received, and expenditures are recorded when cash is paid out. When the cash basis of accounting underlies the preparation of the financial statements, the primary financial statement is the statement of cash receipts and payments. Under the cash basis, long-term assets, accounts receivable, inventory, and prepaid assets are not recognized. Liabilities such as borrowings, accounts payable and accrued charges (e.g. payroll taxes, employee future benefits) are not recognized.

The accrual basis of accounting recognizes the economic effects of transactions and other events when they occur regardless of whether there has been a receipt or payment of cash. Therefore, the transactions and events are recorded in the accounting records and recognized in the financial statements of the periods to which they relate. All assets and liabilities that meet the definitions and criteria for recognition are recognized in the financial statements. Assets and liabilities include items such as accounts receivable and payable and provisions for employee benefits.

When the accrual basis of accounting underlies the preparation of the financial statements, the financial statements will include the statement of financial position, the statement of financial performance, the cash flow statement and the statement of changes in net assets/equity. The elements recognized under accrual accounting are assets, liabilities, net assets/ equity, revenue, and expenses.

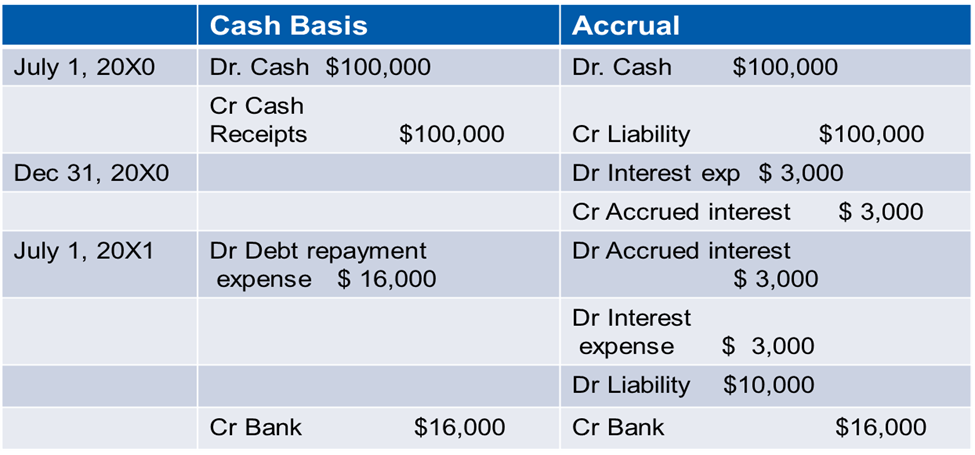

Example of difference between Cash and Accrual Basis of accounting:

Scenario: A Government issues a 10-year debenture of $100,000 with coupon rate of 6 % on July 1, 20×0. Interest and principal are payable annually on July 1. The Government’s fiscal period ends December 31. What are the journal entries to record the transactions under a cash and accrual basis of accounting?

Transitioning to Accrual Accounting

An entity transitioning to accrual accounting is required to develop accounting policies. Initial accounting policies include:

- Valuation methods used to obtain opening balances;

- Transitional provisions in IPSAS applied; and

- Policies for depreciation/amortization and impairment

A successful transition to Accrual Accounting requires:

- A clear mandate – clear mandate from appropriate level of government stating what the reforms will encompass, expected timing and authority of various government bodies to initiate required changes.

- Political commitment – from both governing body, or elected representatives who oversee governing body, and the opposing party is generally required to secure initial approval and provide continuing support when obstacles are encountered.

- Commitment of central entities & key officials – changes to basis of accounting, together with financial management reforms such as devolution of authority for resources, involve changes to power structure; key people who are prepared to publicly stand by changes may also fulfill role officers.

- Adequate resources (human & financial) – identification of types of skills required and planning to ensure availability of those skills is critical to success of transition.

- An effective project management structure – need documented framework/philosophy, formal implementation plan, clear allocation of responsibility, project milestones and procedures for monitoring performance, approval process, formal communication and coordination mechanisms, know where to incorporate additional costs in budget process.

- Adequate technological capacity and IT systems – assess existing systems that link to financial reporting systems; can be a key constraint.

- Use of legislation – provides formal authority for changes and demonstrates governments’ commitment to change.

Summary of IPSAS

The IPSAS standards are as follows:

| IPSAS | Pronouncement | Based on |

| The Conceptual Framework for General Purpose Financial Reporting by Public Sector Entities | N/A | |

| IPSAS 1 | Presentation of Financial Statements | IAS 1 |

| IPSAS 2 | Cash Flow Statements | IAS 7 |

| IPSAS 3 | Accounting Policies, Changes in Accounting Estimates and Errors | IAS 8 |

| IPSAS 4 | The Effects of Changes in Foreign Exchange Rates | IAS 21 |

| IPSAS 5 | Borrowing Costs | IAS 23 |

| IPSAS 9 | Revenue from Exchange Transactions | IAS 18 |

| IPSAS 10 | Financial Reporting in Hyperinflationary Economies | IAS 29 |

| IPSAS 11 | Construction Contracts | IAS 11 |

| IPSAS 12 | Inventories | IAS 2 |

| IPSAS 14 | Events After the Reporting Date | IAS 10 |

| IPSAS 16 | Investment Property | IAS 40 |

| IPSAS 18 | Segment Reporting | IAS 14 |

| IPSAS 19 | Provisions, Contingent Liabilities and Contingent Assets | IAS 37 |

| IPSAS 20 | Related Party Disclosures | IAS 24 |

| IPSAS 21 | Impairment of Non-Cash-Generating Assets | IAS 36 |

| IPSAS 22 | Disclosure of Financial Information About the General Government Sector | N/A |

| IPSAS 23 | Revenue from Non-Exchange Transactions (Taxes and Transfers) | N/A |

| IPSAS 24 | Presentation of Budget Information in Financial Statements | N/A |

| IPSAS 26 | Impairment of Cash-Generating Assets | IAS 36 |

| IPSAS 27 | Agriculture | IAS 41 |

| IPSAS 28 | Financial Instruments: Presentation | IAS 32 |

| IPSAS 29 | Financial Instruments: Recognition and Measurement | IAS 39 |

| IPSAS 30 | Financial Instruments: Disclosures | IFRS 7 |

| IPSAS 31 | Intangible Assets | IAS 38 |

| IPSAS 32 | Service Concession Arrangements: Grantor | IFRIC 12 |

| IPSAS 33 | First-time Adoption of Accrual Basis IPSASs | N/A |

| IPSAS 34 | Separate Financial Statements | IAS 27 |

| IPSAS 35 | Consolidated Financial Statements | IFRS 10 |

| IPSAS 36 | Investments in Associates and Joint Ventures | IAS 28 |

| IPSAS 37 | Joint Arrangements | IFRS 11 |

| IPSAS 38 | Disclosure of Interests in Other Entities | IFRS 12 |

| IPSAS 39 | Employee Benefits | IAS 19 |

| IPSAS 40 | Public sector Combinations | IFRS 3 |

| IPSAS 41 | Financial Instruments | IFRS 9 |

| IPSAS 42 | Social Benefits | N/A |

| IPSAS 43 | Leases | IAS 17 |

| IPSAS 44 | Non – Current Assets Held for Sale and Discontinued Operations | IFRS 5 |

| IPSAS 45 | Property, Plant and Equipment | IAS 16 |

| IPSAS 46 | Measurement | N/A |

| IPSAS 47 | Revenue | IFRS 15 |

| IPSAS 48 | Transfer Expenses | N/A |

| IPSAS 49 | Retirement Benefit Plans | IAS 26 |

| IPSAS 50 | Exploration for and Evaluation of Mineral Resources | IFRS 6 |

| RPG 1 | Reporting on the Long-Term Sustainability of an Entity’s Finances | N/A |

| RPG 2 | Financial Statement Discussion and Analysis | N/A |

| RPG 3 | Reporting Service Performance Information | N/A |

| Financial Reporting under the Cash-Basis of Accounting | N/A |